Credit Cards & Travel Hacking

How To Maximize Travel Using Credit Card Points and Miles

This post contains affiliate links for credit cards for which I may receive bonus points. I only recommend products I use myself.

In my first post on financial literacy, I discussed 5 key tips to successfully leveraging one’s own responsible participation in the economy. In this post, I will further discuss one key aspect - using credit cards to both build your credit and earn personal financial and travel rewards.

This conversation came up because one of the best travel credit cards, the Chase Sapphire Preferred card, is currently offering the highest sign up bonus they’ve ever offered of 100,000 points - and it is expiring this Thursday, May 15, at 9am EDT. The annual fee is $95 and the required spend is $5,000 in three months. A sign up bonus this high hasn’t been available since 2021 (it’s usually 60,000 points), and is the equivalent of $2,000+ in travel credit on partner airlines and hotel chains, or can simply be cashed out for $1,000 cash.

Read on for more details about how to responsibly earn this $1,000+ bonus while boosting your credit score and not spending a penny more than the annual fee.

Responsible Credit Card Usage

Responsible credit card use is often a necessary component of building and maintaining good credit, which saves you money in the long term on unavoidable borrowing costs by showing lenders that you can borrow and dependably pay back money.

In addition to building your credit score, which can lower mortgage and other loan rates - responsible credit card usage should be garnering you rewards like cash back, travel points or miles, and discounts on purchases.

And from a financial security perspective - it is much safer to use a credit card for transactions than to use your personal checking account. If a scammer gets ahold of your personal banking details, they can drain your account and it can be very difficult to get that money back. However, if a scammer gets ahold of your credit card, that concerns the bank’s money, not yours, and it is therefore much easier to block the charges and get a new card issued.

I am of the opinion that if you aren’t using credit cards to your advantage, you’re lowering your credit score, opening yourself up to certain financial risks, and leaving money on the table.

Building Your Credit

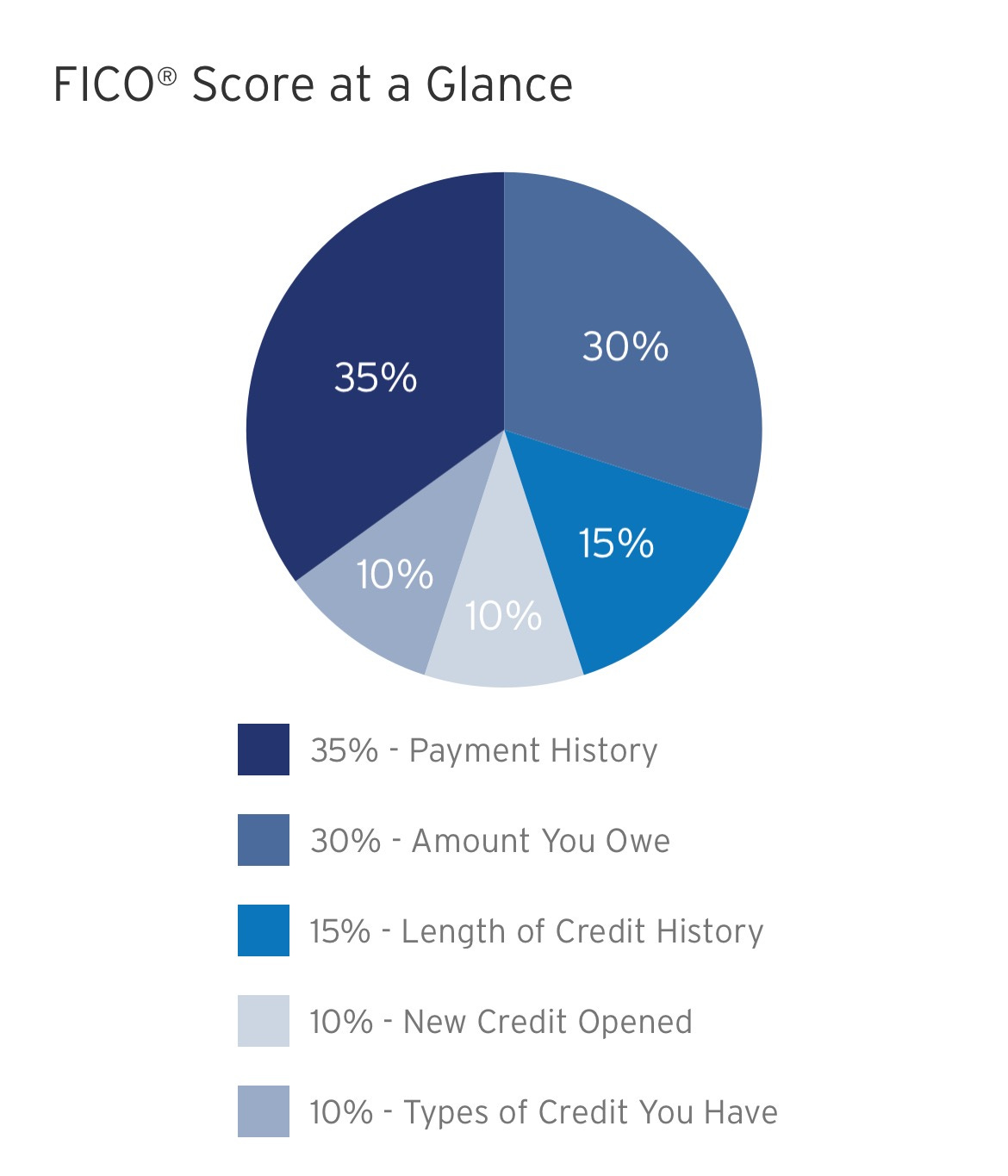

Your credit score is based on a number of factors, weighted as follows:

Payment History (35%) - whether you have paid your credit card bills on time

Pro-tip: ALWAYS pay your entire credit card statement balance every month. Do not carry a balance from month to month. This will avoid interest fees on the charges you put on your credit card.

Credit Utilization (30%) - the amount of money you owe on your credit cards as a percentage of your overall credit limit

Pro-tip: Keep your monthly balance under 20-30% of your total credit limit in order to increase your credit score. For example, if you have a total credit line of $10,000 (not just on one card but across multiple accounts) - keep your spend at or under about $2,000 a month (20%) on your credit cards to maximize your credit score in this area. (And then pay that off every month).

Length of Credit History (15%) - the average length of time all your credit accounts have been open

Pro-tip: NEVER close your oldest credit card. Your overall credit is based on 10 years of history. Your oldest credit card is increasing the average age of your credit accounts. This also means you should make sure the first credit card you open is one you want to keep for a long time (consider low annual fee, good points/miles/reward system, etc.).

New Credit Opened (10%) - the immediate effects of opening a new credit card are slightly negative, as it results in a hard pull on your credit report and lowers the average age of your credit accounts, lowering your credit score - while the longer term effects are positive because it increases your credit limit and, if you pay responsibly, should add a new record of on-time payments to your credit report, increasing your credit score

Pro-tip: Checking your credit score is NOT the same as pulling a full credit report, and will not result in a hard pull on your credit, or impact your credit score at all. I received a lot of questions from people asking how I am regularly monitoring my credit score without lowering my credit score. Your credit score and your credit report are two separate items - your credit score is a simple number and may have a brief explanation attached, while your credit report is a multiple page document with all of the details pertaining to each of your credit accounts over the last 10 years. You can typically view your credit score in many banking and credit card apps, or you can use a free service online, with no negative effect on your credit or credit score.

Credit Mix (10%) - the types of credit you have: credit cards, loans, mortgages

Pro-tip: Don’t take out loans you don’t need, but it is beneficial to have a mix of both revolving credit, like credit cards that are paid off monthly, and installment loans with a fixed repayment schedule, like car loans and mortgages.

Travel Hacking

One of the best things you can do when building credit is making credit cards work for you.

Credit cards are big business - and they compete for your business by offering you points, miles, and even cash back on all your purchases. If you use credit cards responsibly, you can get a lot of rewards and travel benefits for free or at a very reduced cost (just the cost of the annual fee on the credit card). If you’re not a person who travels much, cards with cash back rewards may be more valuable for you.

I have been building my credit with credit cards for over 20 years, and I’ve been using credit cards to offset my travel costs for over 15 years. Here’s how:

The Easy Way

The easiest way to rack up points, miles, or cash is to simply decide what you want (miles on a particular airline, points for a particular hotel group, or cash back) and get a single credit card that gives you the best miles/points/cash per spend on that credit card. Each month, put all the purchases you can on your credit card (avoiding anything that has a credit card fee, if necessary). As you spend money and then pay off the entire statement balance each month - you will begin earning the miles/points/cash you want at no cost to you.

At a minimum, there are credit cards that offer between 1-5% cash back - so if you’re spending $1,000 a month on credit cards, you’re getting up to $50 cash back each month, for free (or for the cost of the annual fee of the card, amortized over 12 months). So you could get $600 cash back each year and with an annual fee of around $100 - that leaves you with $500 extra (tax free!).

The Hacker Way

While certainly valuable, the big credit card rewards aren’t in the monthly spend. The big rewards are in the sign up bonuses. This is what many people who are “hacking” credit cards are doing - regularly opening new credit cards for the lucrative limited-time offer sign up bonuses and leaving them open for at least a year before closing them. It’s called “churning” and it can sound intimidating at first if you haven’t done it before. And it can get you into trouble if you open too many cards, aren’t aware of all the rules, don’t close cards with high annual fees, etc. It’s also a pretty big time suck, and can take away from learning about other ways to maximize your wealth through things like retirement and estate planning.

My Experience

While I do consider myself a bit of a credit card and travel hacker, I am not all in on the “churning” tactics and recommend an approach somewhere in the middle. I currently have just two credit cards open, and for much of my adult life have built my credit score (over 800) and earned lucrative travel rewards with just one credit card - my oldest card that I never close. I stay aware of many of the credit card options out there, and when a good sign up bonus comes along, I will consider opening a new card for just a year to get the bonus.

Our oldest card is an American Airlines credit card, and we have used it to fly for free to destinations all over Europe, South America, Asia, Africa, and North America. When I was too sick to fly, we used our miles for free stays in hotels, including luxury resorts. Because we have had this card for so long and use it for so many purchases, we also have status, which gives us several benefits including free checked bags, access to free premium seat assignments, and priority access to free upgrades.

How Do I Start?

Start by researching the credit card offers that are out there and decide which one would be the most beneficial to you.

Research - Here are some questions to ask yourself in your research:

What’s the best benefit for you - points, miles, or cash back?

Are there cards with benefits on airlines you use regularly?

How about hotel chains you really like?

How much can you expect to earn each month based on your spend?

If that’s in points or miles, what is the cash equivalent?

What’s the annual fee?

What’s the net benefit - cash equivalent of annual points/miles earned minus the annual fee?

What do you get with that annual fee? In addition to the periodic sign up bonuses, many credit cards offer points multipliers on travel and other purchases, access to airport lounges, reimbursed TSA Pre-Check fees, extra travel credits, Door Dash credit, etc.

Choosing the Right Time - Once you have a sense of the cards that will be of the greatest benefit to you, research the sign up bonus the card currently offers, the history of the bonus offers, and the amount you would need to spend to obtain the bonus offer. Consider whether now is a good time to apply (if the sign up bonus is much higher than usual, it typically is):

Are you able to spend X amount in X months?

Sign-up bonuses typically involve you being required to spend a certain amount on the card within a specified time period, like the first three months. Pro-Tip: Opening a new credit card and meeting the minimum spend shouldn’t cost you more than you already spend. Put all your regular expenses on this card: groceries, gas, bills. Plan big purchases - like a couch, other furniture, other travel expenses - for the minimum spend period. Make this your default credit card in your phone, for online purchases, etc.

Apply for the Card - Submit the credit card application and wait for your card to arrive. If you are applying for one of the Chase credit cards, you can call them and have them expedite your card and it will arrive in 1-2 business days.

Chase Sapphire Preferred Card

As I mentioned up front, the Chase Sapphire Preferred card is currently offering the highest bonus offer they’ve ever offered on this card - 100,000 points if you spend $5,000 in 3 months. The sign up bonus is usually 60,000 miles and they’ve only offered 100,000 sign up bonus once before, in 2021. The annual fee on this card is quite low at $95, making it one of the most popular travel cards on the market. This offer is expiring on Thursday, May 15th, at 9am EDT - so if you want this card, I would apply by Wednesday the 14th.

You can use 100,000 points to book $1,250 in travel via the Chase Travel Portal, or you can simply cash it out for $1,000 cash. One of the things that makes Chase credit cards so popular with credit card and travel hackers is that you can also transfer Chase points to 11 airlines and 3 hotel chains that significantly increase the value of the points - increasing it’s value to more than $2,000. These partners include World of Hyatt, Marriott Bonvoy, United Airlines, Air France-KLM, Air Canada, Southwest, JetBlue, and Virgin Atlantic.

If you are looking to start getting into credit cards and travel hacking, this is a great time to start with one of the best and lowest cost cards.

Advanced Tips/FAQs

Many people are working with their spouse or partner in what is called a “Player Two” strategy to increase their collective bonus points. You can maximize your family’s bonus points by signing up for the card, referring your partner, and then pooling your points. With the current Chase Sapphire card bonus, this could increase your earnings from 105,000 (the bonus plus the spend) to 220,000 points:

100,000 sign up bonus

5,000 spend

100,000 partner sign up bonus5,000 partner spend

10,000 referral bonus

= 220,000 pointsIn order to pool points through Chase, you will either need to call Chase and connect the accounts (the two accounts must have the same mailing address) - or you can add each other as an authorized user on the card, which will allow you to transfer the points to either person’s partner airline/hotel accounts.

Another strategy people employ is getting business credit cards for the sign up bonuses. It does not take much to apply for a business credit card as a sole proprietor - many companies do not require an EIN and let you apply with your SSN. Business credit cards may or may not appear on your personal credit report.

One thing to keep in mind with Chase in particular is the 5/24 rule - you cannot open more than 5 credit cards in 24 months. Business credit cards don’t count towards this.

Another rule that impacts those using the popular Sapphire cards is that you can only get one sign up bonus every 48 months. The last time the Chase Sapphire bonus of 100,000 miles was offered was summer of 2021 - just under 48 months ago, so anyone who received the bonus then is not eligible for the bonus offered now.

It can become addicting to game the system and rack up travel points and miles, but don’t forget to balance getting locked into one system while still allowing yourself the flexibility to book with other airlines/hotels if you want. I personally use a lot of American Airlines miles and World of Hyatt points - but I often find better flights paying cash with other airlines, and Marriott has more hotels that are cheaper to pay with cash (and their points system isn’t as lucrative). So I balance all these things to get the best travel deal possible, without staying locked into just my points. This is why it can be valuable to keep a card after a year because you’re still passively getting miles/points on each spend, once the sign up bonus is long gone.

Knowing when to close a credit card and how it will impact your credit is critical. Unless you are very good at managing all your cards through a spreadsheet and want to dedicate a lot of time to tracking net benefits, I don’t recommend keeping that many credit cards open. It’s better to close a card after a year than keep it open and keep paying the annual fee when you aren’t reaping any benefits. Contrary to popular belief, closing a credit card after a year does not necessarily hurt your credit. As previously discussed, opening a credit card can have a slight negative impact on your credit because it results in a hard credit pull and it drops the average age of your cards. Closing your oldest credit card will also drop the average age of your cards, which will result in a negative impact. But in most cases, closing a newer card will result in a minimal or short term drop in your credit score of a few points. The significance of the impact of closing a credit card depends on your overall credit:

How many cards you have

Average age of cards

Total debt ratio

If you are buying a house and applying for a mortgage, or buying a car - it is NOT a good time to open a credit card.

What’s the Catch?

So now you may be asking yourself - why are banks offering these credit card deals that have such good bonuses, worth much more than the annual fee? Well, because they are banking on you screwing up. If you carry a balance for just one month, at a 20-30% APR, that can end up costing more than the sign up bonus they offered you. If you pay a second year of annual fees, because you forgot to cancel or even because you decided to keep the card, that can cover the cost of the sign up bonus as well, depending on the amount of the annual fee and number of years you keep the card.

But if you, like me, struggle with balancing lifelong hyper vigilance - you won’t screw up. You’ll set up an auto-pay to pay the entire balance of your credit card statement every month out of your checking account. You’ll make a spreadsheet calendar of when you need to cancel before the second annual fee hits. You’ll put alerts in your phone as a back up to ensure you don’t get got by some bank.

If you keep in mind all of the above, you can have a credit score over 800 and free travel benefits at a very low cost.

Love this, so many awesome tips here!

Also if you’re like me and forget, you can immediately call the credit card company and get them to reverse the charge and either close the account or downgrade to a no fee card. But it’s definitely better to get ahead of it